Or, they might have now been. The nearby garish strip shopping mall has an even more subdued but similarly treacherous neighbor, anchored by your own finance business called Regional Finance. Providing loans on slightly longer terms guaranteed by items for your home as opposed to paychecks, individual boat finance companies aren't susceptible to Southern Carolina’s new cash advance guidelines. In reality, the payday reforms appear to possess spurred their development. Advance America consolidated the state’s cash advance market into the wake regarding the regulations that are new and industry watchdogs suspect that competitors, like Check ‘n Go, have actually relicensed on their own as personal boat finance companies.

Like its rivals, Regional delivers mailers to area households with checks for pre-approved loans. In July 2010 Elsie accepted one for $446; she’ll spend $143 in finance fees within the lifetime of the mortgage. Sam took one out too, in December 2009, to get Christmas time gifts. Elsie can’t remember why she took hers, nevertheless when pushed each of them mumble about being too substantial and fret that every thing simply seems higher priced today. Both had been surprised whenever told which they did from the  payday lenders they despise that they got the same deal from Regional.

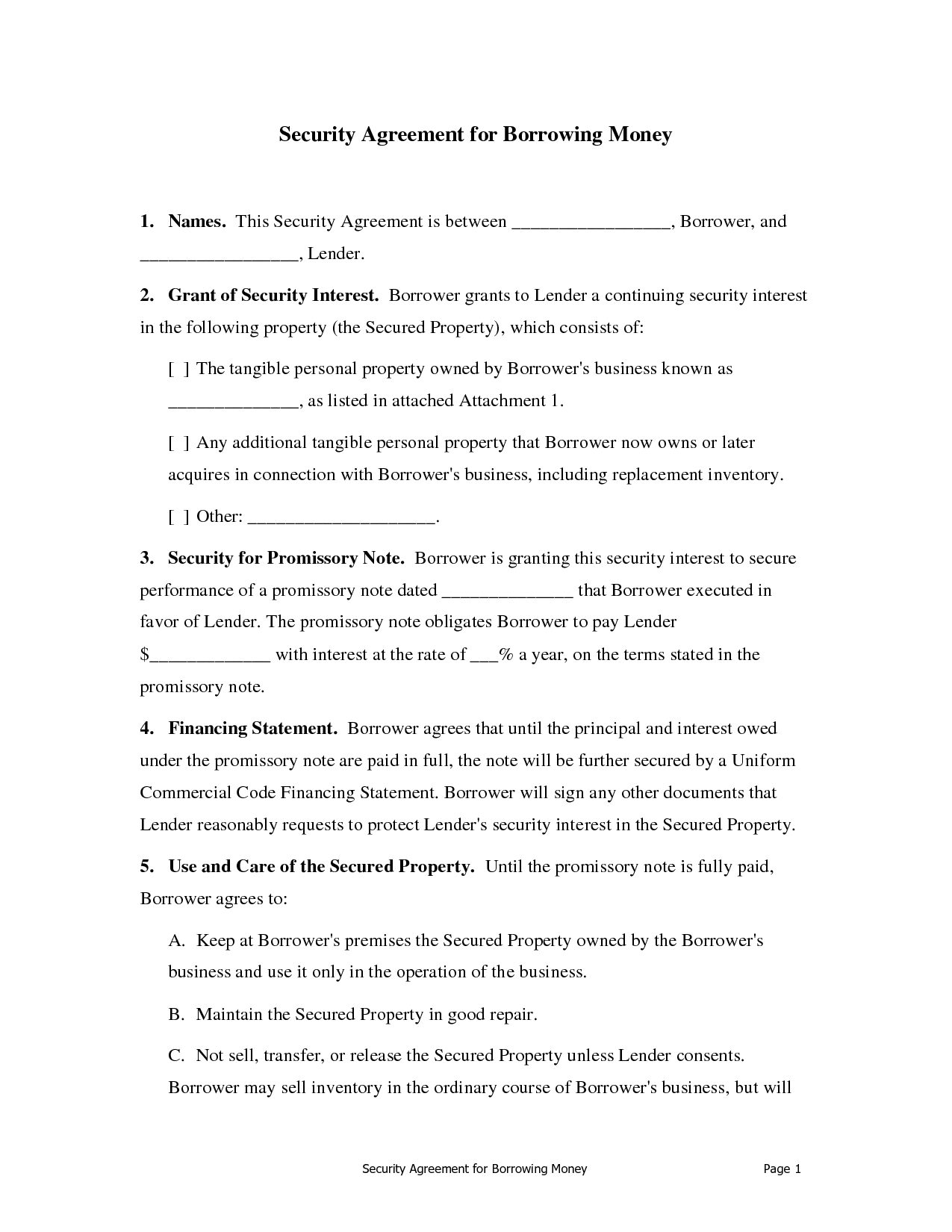

payday lenders they despise that they got the same deal from Regional.

“They have been through this period again and again, ” claims a frustrated Pena. “I’ve tried to teach them, and they’re the sweetest people, nevertheless they simply don’t obtain it.

The finance companies are an improvement in some ways. The loans flip less often since they are generally for three to eighteen months, perhaps maybe not fourteen days. Nevertheless the concept continues to be the same: that loan for under $1,000 with costs that result in incredibly high interest levels that may be flipped in regards to due. For Hawkins, these loans prove a easy point about subprime customer lenders of most stripes. “There’s just one method to dispose of those, ” he claims. “And that’s to pull it out root and branch. ”

Certainly, states which have attempted to control high-cost customer financing are finding it a full-time work. In state after state, payday loan providers who encountered brand new guidelines just tweaked their companies without changing the core model. Since 2005, for example, Advance America among others have recast by themselves as credit fix companies in states that maintained interest caps on nonbank lending. Particularly, this started following the FDIC banned lenders that are payday partnering with out-of-state banking institutions to evade price caps. They charge a debtor a typical payday financing cost, then link the debtor having a third-party loan provider who finances the small-dollar loan at a rate that is legal. In accordance with Weed, it is legal in twenty-six states.

Variants with this theme are array. Whenever Ohio capped rates of interest in 2008, Advance America started providing payday loans under a home loan lender permit. Whenever Virginia tightened payday financing guidelines in 2009, the business began providing loans as open-ended personal lines of credit, before the state regulator stepped in. In brand brand brand New Mexico, following the state passed a apparently strict pair of laws, lenders created longer-term installment loans just like those of South Carolina’s finance organizations and, in accordance with a report by University of the latest Mexico appropriate scholar Nathalie Martin, transferred clients straight into the latest regulation-free loans without informing them. Others offered payday advances without going for a check as protection, an adjustment that put them outside regulatory bounds.

Loan providers also have just ignored regulations. After new york passed its 36 % interest limit in 2003, a consumer team filed a lawsuit that is class-action centered on a study because of the attorney general’s workplace, recharging that Advance America went directly on financing at triple-digit prices.

Advance America additionally assures its Wall Street investors so it’s maintaining the changing regulatory weather by checking out new services. It started providing debit that is prepaid, and also by 2009 it had significantly more than 167,000 cards full of $374 million. In 2007 it partnered with MoneyGram to supply cable transfers in its stores. In late 2008 it launched a web-based payday application that logged 95,000 new loans with its very very first 12 months.

Customer advocates say all this work indicates one solution: a cap that is federal nonbank customer financing just like the the one that went into impact for solution people in 2007. President Obama promised to take action during their 2008 campaign, and Senator Dick Durbin introduced bills in 2008 and 2009 that will have produced a 36 per cent limit, a come back to previous laws that are usury. Advance America is dull regarding how that will influence its company. “A federal legislation that imposes a nationwide limit on our charges and interest may likely eradicate our capability to carry on our present operations, ” declares its 2010 yearly report.

The Congressional price limit discussion ended up being displaced, but, because of the hot debate throughout the 2010 economic reform legislation, which dealt with all the concern by making a brand new consumer-protection watchdog. Congress granted this new customer Financial Protection Bureau (CFPB) oversight for the previously unregulated nonbank loan providers, including payday loan providers. But which was mainly inclined to the home loans which had pressed subprime house refinances, as well as the bureau is mainly embroiled in a debate over exactly how much authority it has over Wall Street banking institutions. With every industry that is financial lobbying difficult to limit the bureau’s authority, CFPB should be able to police just countless products, and very very early reports recommend it will probably pay attention to mortgages. When it comes to payday loan providers, the bureau is anticipated to spotlight customer education and disclosure that is enforcing. In state efforts, neither has proven a counterweight that is effective the industry’s saturation of working-class areas with predatory services and products.

Disclosing payday lenders’ APR has done small to greatly help borrowers such as the Blacks because, claims Pena, the mathematics of these economic life does not mount up. “ When anyone are hopeless to cover some other person, and this type of person calling me personally and harassing me personally and so they want $300 and, whoops, look what I got in the mail today…” She throws up her hands at what happens next today.

For the Blacks, Pena includes a feeling that is sinking what’s next. Neither of those is healthier, and Sam concerns just what will take place if one of them results in a medical house, or even even worse. He’s asked Pena to check in to a reverse mortgage with their home, which will make sure they could remain they both die in it until. Pena’s perhaps not positive they have that it will work out, given how little equity. These are typically one health crisis far from homelessness.

“I’m winding down my career, ” Pena claims. “And I was thinking whenever I found myself in this industry twenty-something years ago that things would now be better by. However they are in reality even worse, due to the various items that have already come out. ” It accustomed you need to be bank cards, that was one thing she comprehended. Now, she states, she scarcely recognizes the finance world that is personal. “I don’t know—the economic globe simply got greedy and went cuckoo. ”

Additionally in this problem, Adam Doster states on a brand new option to payday advances that is being tried in Baltimore.

Kai Wright Twitter Kai Wright is host and editor of WNYC’s narrative unit, and a columnist when it comes to country.

To submit a modification for the consideration, follow this link.